The volatility of the couple or the week has achieved the importance of assets. Capital protection and diversification play a primary role in the successful investment trip. And what better way to do it than with a sovereign instrument backed? Here we take a look at the Floating Rate Savings Bonus of the Indian Government (FRSB) and the guide if it does.

Interest rate

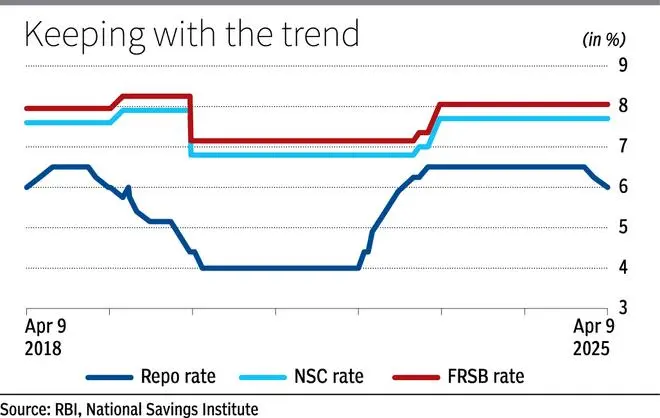

The FRSB are the bonds with interests issued by the government of India, reimbursable after 7 years. The interests are paid half a year on January 1 and July 1 of each year. Since these are floating rate bonds, the interest rate is restored every six months (January 1 and July 1), with a 35 -point cousin (BP) at the prevailing rate of NSC (national savings certificates). Currently, the interest rate in NSC is 7.7 percent and, therefore, the applicable rate for FRSB is 8.05 percent.

The NSC is also an instrument supported by the government that matures after five years. There are a couple of things that fundamentals differentiate the FRSB of the NSC. First, the interest rate in NSC is set during the entire tenor of five years unlike the FRSB and, therefore, investors can block the rate of performance at the time of opening the NSC account. The interest rate for NSCS is checked quarterly, depending on the average 5 -year government security yield. Second, the accredia of interest after the year in the NSC is cumulatively reimbursed only by maturity.

How can you buy

A great feature that differentiates FRSB is that they are available as a touch as outdated aginst values, whose problems follow a fixed schedule. Investors can approach their banks or use the RBI Retail Direct platform to buy FRSB. Some banks also take requests in their net bank portals. The minimum required investment is ₹ 1,000, which also turns out to be the nominal value of a bonus and can be increased by multiples of ₹ 1,000. There is no limit in the maximum amount you can invest.

Taxes and other terms

FRSBS interests are subject to ashes for applicable taxes. TDS is applicable. However, one can obtain a TDS exemption by sending form 15g or 15h. Only residents and HUFs are eligible to invest in FRSB. There is no age bar, except, in the case or minors, guardians can invest in representation or minors. Nomination and joint participation are allowed. FRSBs are transferable to Neinder or can be used as a guarantee for loans.

Packing

Premature coverage is allowed. Investors who are 80 years or older can be withdrawn after a four -year block, between 70 and 80 can be withdrawn after 5 years and those of 60 to 70 can be withdrawn after 6 years. Age on the date of premature collection is relevant and not the age on the date of investment. In the case of joint tenure, at least investors must comply with the age criteria.

However, a point to keep in mind is that the amount of redemption (main with interest calculated after deducting the fine) will be only on the interest payment date after the premature collection date. For example, if the premature wrapping is applied on August 31, the redemption processes will be accredited only on January 1. The fine is calculated as half of the interests owed and payable during the last six months of the tenure period. In the previous example, the fine will be 50 percent of the interest payable for the period from July 1 to December 31.

It is possible a partial premature charge, if the amount of the investment had been divided and invested in multiple applications. That is, if it is said that ₹ 1 Lakh is reversed in two requests of ₹ 50,000 each, then you can request premature coverage of bonds under any of the applications, while the other continues maturity.

Our shot

The 7 -year -old tenor is long enough to accommodate multiple cycles of interest rates.

Cycles have a shorter and in the past seven, we had a rate (Repo Rate) hike cycle from august 2017 to August 2018 (6 to 6.5 per cent), to period of constant rates until january 2019, a rate downcycle till May 2020 (6.5, rate), artal percot), Rate Perch), Rate Perch), Rate Perch), Rate Perch), Rate Per Cent), Rate Perch), Rate Per Cent), Rate Perca), Rate percent), Perca Rate), Rate percent), Rate percent), Rate), Rate percent), Rate), Rate percent), March. From May 2022 to February 2023 (4 to 6.5 percent), constant rates until January 2025 and the posterior rate cycle from February (6.5 to 6 percent so far). Given this observation, it would be safe to assume that the continuous rate reduction cycle may not last the complete tenor of a seven -year FRSB.

The monetary market is influenced by many variables and is quite difficult to tame the cycles of walks and low cycles. In this context, a key limitation of a term deposit or any product that allows it to block the interest rate for the tenor of the investment is that these products suffer the risk of reinvestment, the risk that rates can be lower when you want the expiration of the expiration. Currently, the bank sacrifices the highest rates in FDS for tenors that exceed a year and no more than 3 years. Interest rates could be lower when such mature FD. With FRSB, you can rest easily as the rates are restored every six months, allowing you to enjoy the rates cycles when they occur.

The interest rate in FRSB is based on the government rate pays to the NSC. An analysis of NSC rates in the last 10 years reveals an average extension of 62 bp on 5 -year G -SEC yield, with a range between -35 bp and 163 bp. With another 35 bp extended by the NSC rate, the FRSB could deliver inflation beaten yields, while capital remains insured by a sovereign guarantee.

The investors and citizens of the elderly, of course, the FRSB of the candidates can complement the income of other investments, such as the annuity of NPS, the bank FD, the monthly income scheme of the post office and the savings scheme for the elderly.

Posted on April 19, 2025